The average Aussie will change careers twice in 20 years – not just jobs, but whole professions.

AI, demographics & economic shifts are reshaping industries faster than ever.

The winners will be those who embrace lifelong learning & human skills like creativity, empathy, and adaptability.

Employers that invest in reskilling will keep their best people—and thrive.

A non-linear career path is no longer a weakness—it’s a competitive advantage.

Imagine this: you’ve built a career, perhaps even become an expert in your field, and yet in the next 10 or 15 years, you will find yourself doing something entirely different.

Not just working for a new boss or switching companies, but stepping into a completely new career.

That’s not science fiction, it’s the forecast for the average Australian worker.

On current trends, we’ll completely change occupations more than twice in the next 20 years.

This raises some important questions: what’s driving this shift? How can we prepare for it?

And perhaps most importantly, how can we ensure these changes become opportunities rather than disruptions?

For weekly insights subscribe to the Demographics Decoded podcast, where we will continue to explore these trends and their implications in greater detail.

Subscribe now on your favourite Podcast player:

Why this matters

Once upon a time, work was predictable.

You studied, entered a profession, stuck with it for decades, and retired with a handshake and maybe a gold watch.

Today, that idea looks as outdated as a typewriter.

As Simon Kuestenmacher, leading demographer and my co-host on Demographics Decoded, points out:

“Change is a good thing. It is scary, which is why we don’t do it. But ultimately, as individuals, we’re cheating ourselves out of opportunities when we avoid it. And as a country as a whole, we’re cheating ourselves out of productivity.”

This is about more than personal careers, it’s about national competitiveness.

If Australians can adapt, reskill, and reinvent, our economy thrives.

If we resist change, we risk falling behind.

What’s driving career change?

Several powerful forces are reshaping the world of work:

1. Technology and AI

Automation is already replacing routine tasks in industries from banking to retail.

Roles like data entry clerks, postal workers, and even some accounting jobs are shrinking rapidly.

At the same time, entirely new roles are emerging: AI specialists, big data analysts, fintech engineers, and developers in fields we haven’t even named yet.

Simon draws the parallel to the Internet revolution:

“In the late 90s, everyone had an email address, but we hadn’t conceptualised social media or online retail yet. We are now at this point with AI. We know it’s big, but we don’t yet know all the jobs it will create.”

2. Demographics

Australia’s workforce is ageing.

As baby boomers retire, they’ll leave a huge vacuum of roles to be filled.

With fewer younger workers coming through, industries will increasingly welcome career shifters.

Healthcare and aged care, for example, are doubling in size and will need vast numbers of new workers, many of them transitioning from other industries.

3. Economic Shifts

As the economy restructures, workers must follow the opportunities.

The decline of manufacturing and fossil fuels contrasts with the rise of renewable energy, logistics, and technology.

Career pivots aren’t optional, they’re survival.

4. Globalisation & Migration

Changes to global supply chains, plus Australia’s migration policies, will continue to shape the job market.

If managed well, migrants can fill skills shortages while locals pivot to new roles.

But if handled poorly, it can create unnecessary competition and tension.

The barriers holding Australians back

Ironically, even though the economy needs more labour mobility, Australians are less likely to change jobs today than in the 1990s.

Why? Housing affordability.

“In the past, changing jobs often meant changing cities,” Simon explained. “But with housing being so hard to come by, and people being stuck in mortgages for 30 years, we’re less willing to take risks.”

Add to that the fact that most households now rely on two incomes.

Moving cities doesn’t just mean one person finds a new job; it means two people do. That level of uncertainty keeps many families locked in place.

So while technology is pushing us towards change, structural realities are pulling us back.

Preparing for the future of work

The message is clear: career change is no longer the exception; it’s the rule.

Here’s how to prepare:

1. Adopt lifelong learning

Gone are the days when a degree set you up for life.

Workers need continuous, bite-sized upskilling.

Simon argues for “micro-trainings and bootcamps” that let workers pivot quickly without taking years out of the workforce.

2. Develop Human Skills

Technical knowledge expires quickly.

The real differentiators are human skills: adaptability, communication, creativity, problem-solving, empathy, and proactive time management.

“Always double down on human-centric skills,” Simon advised. “Figure out what humans do better than machines, and focus on those.”

3. Combine Disciplines

The most valuable workers will be those who can bridge industries, bringing medical expertise into tech, for example, or combining data analytics with social sciences.

These hybrids stand out.

4. Leverage AI for Learning

Rather than fearing AI, we should use it.

Schools and companies are already experimenting with personalised learning journeys tailored to each student or employee.

This will make reskilling faster, cheaper, and more effective.

Who risks being left behind?

Not everyone is equally prepared for this future.

Workers in regional towns, those with lower formal education, and older workers are at greater risk of being stranded as industries evolve.

Simon doesn’t sugarcoat it:

“If a certain kind of industry becomes obsolete and you don’t pivot, you sit there economically unproductive, frustrated, and left behind. You must change.”

That’s why governments, employers, and education providers need to work together to smooth transitions.

A fragmented system that leaves mid-career workers without quick reskilling options will only deepen inequality.

The role of employers

At Metropole, I’ve always said our biggest asset is our people.

Employers must invest in their teams, not just for productivity, but for retention.

Some worry about training staff who might leave.

My view is the opposite: I’d rather train them and give them a culture worth staying for.

As Simon put it:

“If improving your staff makes them want to leave, that doesn’t speak well for your organisation.”

In today’s tight labour market, being an employer of choice is no longer optional, it’s survival.

The upside of career change

For all the fear around disruption, there’s a strong silver lining.

Many people who’ve been forced into a new career later admit it was the best thing that ever happened to them.

Younger generations, shaped by the pandemic, are arguably more resilient and adaptable than ever.

They expect change, and that mindset may prove to be their greatest asset.

And perhaps most importantly, employers and society are beginning to value non-linear career paths.

Having a zigzagging resume is no longer a weakness, it’s a strength.

Final thoughts

The future of work in Australia will be defined by movement, between roles, industries, and even entire professions.

It’s no longer realistic to expect a straight-line career.

The real question is: will you resist the shift and risk being left behind, or will you embrace it as a chance to reinvent yourself?

Because while career change may be unavoidable, it doesn’t have to be negative.

With the right mindset and preparation, it could well be the best thing that happens in your working life.

If you found this discussion helpful, don’t forget to subscribe to our podcast and share it with others who might benefit.

Subscribe now on your favourite Podcast player:

About Michael Yardney Michael is the founder of Metropole Property Strategists who help their clients grow, protect and pass on their wealth through independent, unbiased property advice and advocacy. He’s once again been voted Australia’s leading property investment adviser and one of Australia’s 50 most influential Thought Leaders. His opinions are regularly featured in the media.

A new apartment complex planned for Oxford Street in Bondi Junction should be a textbook example of smart city development.

The Bondi Junction project is exactly the kind of housing Australia needs: well-located, near transport, jobs, schools, shops, and open space.

Yet it faces delays from complex approval processes, including both NSW planning rules and the Federal Environment Protection and Biodiversity Conservation Act.

Sydney lost over 41,000 residents in 2023–24, many young people leaving due to unaffordable housing.

Without more supply in high-demand areas, inequality will deepen and cities risk losing their younger generations.

A new apartment complex planned for Oxford Street in Bondi Junction should be a textbook example of smart city development.

Sixteen storeys of housing, right next to a train line and bus routes, within walking distance of Centennial Park, Bondi Beach, shops, jobs, schools, and even the harbour.

On a site currently occupied by a car rental yard, it would convert low-value land into dozens of homes where people actually want to live.

And yet, this project is shaping up to be a case study in why Australia struggles so badly to build enough homes.

The approvals maze

Despite there being no historic or cultural heritage concerns on the site, the developer still has to secure approval not just from the NSW planning system, but also the Federal Government under the Environment Protection and Biodiversity Conservation Act.

Environment Minister Murray Watt has acknowledged the Act is cumbersome and outdated, promising reform by year’s end.

At last count, around 30,000 housing and construction projects were waiting on approvals under this federal law.

That’s tens of thousands of homes delayed while Australia faces a rental crisis, soaring house prices, and widespread affordability pressures.

NIMBY pushback from wealthy areas

The second major hurdle is local opposition.

Sydney’s eastern suburbs are among the wealthiest in the country, but they’re also among the most resistant to change.

Residents argue the towers will cast shadows over Centennial Park and hurt local character.

Former Sydney Morning Herald editor Darren Goodsir, now a senior university executive, submitted that such developments “favour profit-driven ventures” and risk creating a housing market for the wealthy.

But let’s be blunt: Sydney’s eastern suburbs are already one of the wealthiest housing markets in Australia.

Blocking new housing there doesn’t create affordability, it entrenches exclusivity.

The official custodians of Centennial Park themselves said the impact would be minor: a sliver of extra shadow for about an hour on one winter morning. Hardly a biodiversity crisis.

The YIMBY response

This fight has triggered a sharper response from Sydney’s emerging YIMBY (Yes In My Backyard) movement.

Their argument, backed by economists like former RBA researcher Peter Tulip, is straightforward: every new home helps.

Even if a new apartment isn’t cheap, the person who moves in frees up another home for someone else.

Over time, that chain reaction eases pressure across the whole market.

Limiting supply, on the other hand, only drives up prices and rents further.

As one Sydney YIMBY post put it: “Step 1: Engineer a housing crisis by blocking new homes. Step 2: When somebody proposes building homes, complain they’re not affordable. It’s just so unbelievably self-serving.”

Governments are still fuelling demand

The supply bottleneck wouldn’t be so severe if governments weren’t simultaneously pouring fuel on the demand side.

Recently the federal government brought forward its first-home buyer subsidy program.

What was once capped and income-tested is now open-ended, no income test, no limit on places.

That means more buyers with extra purchasing power competing for the same stock of housing.

In fact, it is suggested that 70,000 new first-home buyers will take advantage of this scheme in the first year.

And as economist Saul Eslake dryly observed, governments keep doing this because voters want house prices to rise faster than incomes.

It’s a political cycle: homeowners vote for higher property values, governments deliver, and affordability for younger generations slips further out of reach.

The social cost of Nimbyism

The bigger picture is stark. Sydney lost over 41,000 residents last financial year, many of them young people priced out of their birthplace.

They’re moving to more affordable parts of the country, taking their skills and spending power with them.

Meanwhile, councils like Woollahra continue to oppose densification, even arguing that new apartments would be “unaffordable.”

But refusing to build more homes in high-demand areas ensures prices stay elevated everywhere.

As NSW Premier Chris Minns put it, too many communities have embraced a “culture of no.”

The result is fewer people living in well-connected suburbs than in the 1970s, despite decades of population growth.

Some final thoughts

The Bondi Junction saga highlights everything wrong with our housing system: over-regulation, self-interested local opposition, and political incentives that prioritise rising values over affordability.

If we’re serious about fixing the housing crisis, we can’t just throw subsidies at buyers or leave planning power in the hands of those who already own homes in exclusive postcodes.

We need planning reform, faster approvals, and a willingness to build more homes in the places where people want to live.

Because without change, Sydney and other capitals will keep losing their young people, and with them, their future.

About Chris Dang Chris Dang is an accountant by training and has worked in the Financial Planning industry for many years. Chris brings together property, accounting, and financial planning experience to help clients of Metropole Wealth Advisory create a holistic plan for their wealth.

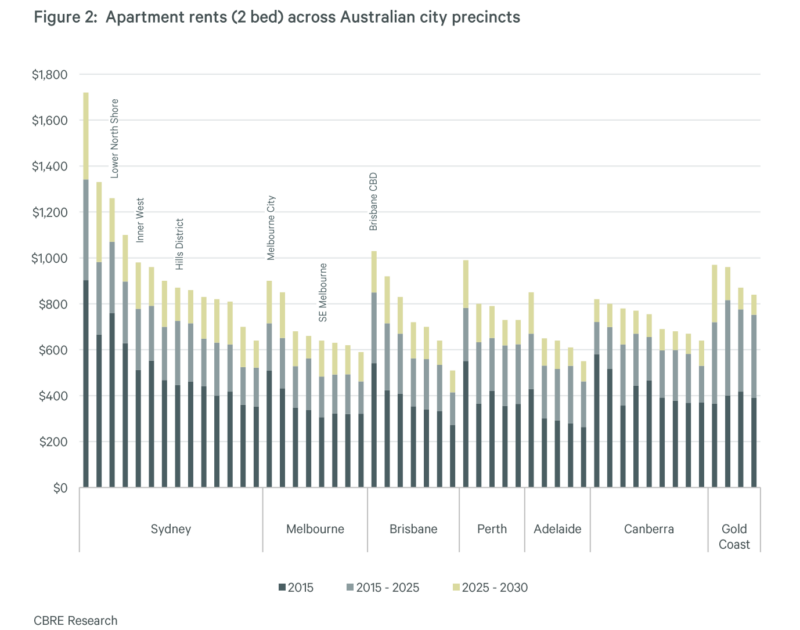

Median apartment rents across Australian capitals are forecast to rise 24% between 2025 and 2030.

By 2030, 92% of 2-bed apartments will cost more than $700/week, with one-third topping $1,000/week.

Renters will continue to face affordability challenges as demand heavily outstrips supply.

Median apartment rents are likely to grow by 24% between 2025 and 2030, across Australian capital cities, according to the latest report by International Property Consultancy, CBRE.

By 2030, 92% of 2-bed apartments are forecast to have rents exceeding $700/week (33% exceeding $1000/week).

CBRE expect that capital city vacancy rates will fall further to 1.1% by 2030 from 1.8% in 2025.

These tight conditions will endure as vacancy stays at around half of the previous decade’s average of 2.5%.

The report highlights how newly built apartments trade at a premium to older vintages.

For example, newly built two-bedroom apartments are at a 30% price premium to older apartments.

High construction costs and better amenities have also put upward pressure on rents for new builds.

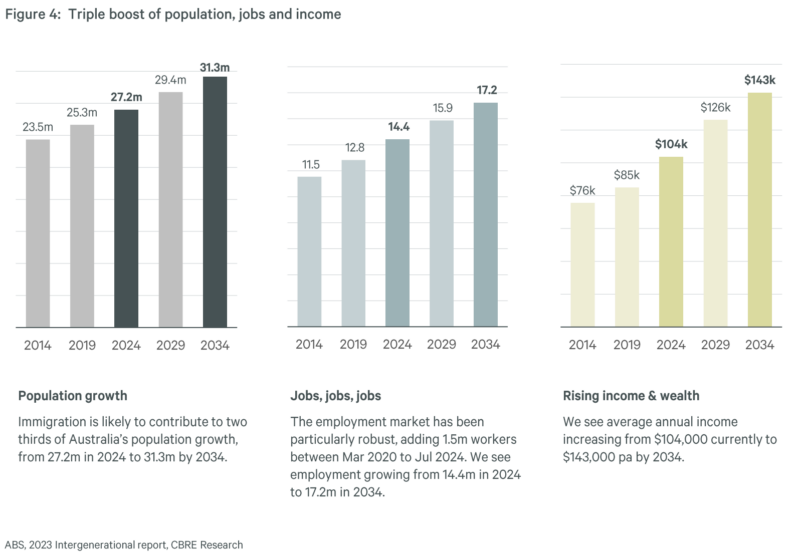

Over the next 10 years, demand for housing is expected to benefit from a triple boost: rising population (+4.1 million), rising jobs (+2.8 million), and rising income (+$39k).

CBRE estimates around $960 billion of additional income in the system to support mortgage, rent, and other living expenses.

According to the report, after accounting for on-costs such as municipal rates and strata fees, it is cheaper to rent in all precincts across Australia.

Monthly rents are 30-40% cheaper than alternative buy options at current prices.

CBRE forecasts the future supply of apartments is likely to hover around 60,000 p.a. over 2025-30.

However, Australia’s projected population growth necessitates an apartment supply of approximately 75,000 annually to prevent further declines in vacancy rates.

Sydney: Apartment delivery will average 11,700 p.a. over 2025-30, well below 30,000 p.a. demand for total housing stock. Vacancy rates are set to fall from 2.0% to 1.2%.

Melbourne: Apartment delivery to average 9,000 p.a. over 2025-30, nearly 25% below Sydney. Demand for housing stock (apartments and communities) is expected to average 38,000 units per annum over the next five years. This should continue to drive down city-wide vacancy from 2.1% to 1.4%.

Brisbane: Apartment delivery to average 4,600 per annum over 2025-2030. Demand for housing stock (apartments and communities) is likely to average 16,000 p.a., which will drive down city-wide vacancy from 1.1% to 0.7%.

About Leanne Jopson Leanne is National Director of Property Management at Metropole and a Property Professional in every sense of the word. With 20 years’ experience in real estate, Leanne brings a wealth of knowledge and experience to maximise returns and minimise stress for their clients.

Have you ever wondered why some property investors seem to build multi-million-dollar portfolios while others never get past their first property—or worse, sell up within five years?

It’s not about luck. It’s not about earning six figures. And it’s definitely not about being born into money.

In today’s podcast, I explore the common myths surrounding wealth creation and property investment with Brett Warren

You’ll learn that most people are trapped by money myths – false beliefs about wealth, investing, and financial security that sound logical but quietly sabotage their success.

So we explore 15 of the most common wealth myths holding Australians back.

If you’re serious about building financial freedom, this episode will challenge the way you think about money and give you the insights to move forward with confidence.

Takeaways

Many people are held back by limiting beliefs about money.

Taking action is crucial for financial success.

Financial independence requires understanding and planning, not just a high income.

Debt can be a tool for wealth creation if managed properly.

Investing is a process that requires strategy and knowledge.

Mindset plays a significant role in achieving financial goals.

There are always opportunities in the property market, regardless of timing.

Diversification can lead to average outcomes; focus on mastering one area first.

Home equity can be leveraged to invest in additional properties.

Having a support team can enhance your investment journey.

Also, please subscribe to my other podcast Demographics Decoded with Simon Kuestenmacher – just look for Demographics Decoded wherever you are listening to this podcast and subscribe so each week we can unveil the trends shaping your future.

Subscribe & don’t miss a single episode of Michael Yardney’s podcast

Hear Michael & a select panel of guest experts discuss property investment, success & money related

topics. Subscribe now, whether you’re on an Apple or Android handset.

Need help listening to Michael Yardney’s podcast from your phone or tablet?

We have created easy to follow instructions for you whether you’re on iPhone / iPad or an Android

device.

Prefer to subscribe via email?

Join Michael Yardney’s inner circle of daily subscribers and get into the head of Australia’s best

property investment advisor and a wide team of leading property researchers and commentators.

About Michael Yardney

Michael is the founder of Metropole Property Strategists who help their clients grow, protect and pass on their wealth through independent, unbiased property advice and advocacy. He’s once again been voted Australia’s leading property investment adviser and one of Australia’s 50 most influential Thought Leaders. His opinions are regularly featured in the media.

The Monash Institute of Transport Studies found the Gold Coast is operating 14% above its ideal capacity, making it the nation’s most overpopulated city.

Other overstretched areas include the NSW Central Coast (13%) and Murray Bridge in South Australia (12%)

Researchers defined a city’s ideal size based on capital city status, job access, service mix, and connectivity.

Cities within 4% of their “just right” size save renters an average of $1,560 per year, reduce car dependence, and allow more people to walk to work.

Rents are among the least affordable in Queensland, with almost no options for low-income earners or those on income support.

Despite stress, demand remains strong due to lifestyle appeal, hybrid work, migration, and upcoming Olympic investment.

Prices are likely to continue rising, but affordability challenges and infrastructure strain present risks that investors must factor in.

Investors will find better long-term opportunities in Brisbane.

What happens when your dream holiday destination turns into a staging ground for gridlock, sky-high rents, and near-invisible housing options?

Welcome to the Gold Coast—a city fighting to catch up with its own popularity.

It was once known for its glittering beaches, holiday resorts, and laid-back lifestyle, but today, the Gold Coast has earned a very different title: Australia’s most overpopulated city.

The study measured 655 Australian cities and found that the Coast is currently sitting at around 14% above its sustainable capacity.

In practical terms, that means clogged highways, longer commutes, skyrocketing rents, and a housing market that’s almost outpacing Sydney.

What was once Australia’s playground has now become a city under strain.

What makes a city “too big”?

The researchers weren’t just counting heads.

They looked at four factors that make cities tick:

Whether it’s a capital city,

Access to jobs,

The mix of services available,

And how well-connected the city is.

They found that when a city grows too big, the warning signs are obvious: traffic jams, overcrowded services, and housing that becomes unaffordable for the very people who keep the city running.

But interestingly, cities that were closer to their “just right” size delivered tangible benefits.

Renters saved an average of $1,560 a year, more people could walk to work, and hundreds of thousands of households needed fewer cars.

So, it’s not about size alone; it’s about balance.

Growth outrunning infrastructure

On the Gold Coast, demand has simply run ahead of supply.

Population growth, fuelled by lifestyle demand and interstate migration, has outpaced the infrastructure meant to support it.

Property prices tell the story clearly.

The median house price on the Gold Coast has surged to $1.32 million; the only regional market in Australia where prices outstrip its capital city.

Over the past year, prices have jumped nearly 9%, more than double the pace of Sydney.

And it’s not just buyers feeling the squeeze. Renters are under severe stress too.

A recent report revealed “close to zero affordable options” for low-income earners, with conditions deteriorating further over the past 12 months.

Note: The Gold Coast is now the least affordable rental market in Queensland.

Why this matters beyond the Gold Coast

You might be thinking: “Well, that’s the Gold Coast, what about the rest of the country?”

But the truth is, this isn’t just a local problem.

Other areas like the NSW Central Coast, Murray Bridge, Sydney, Melbourne, and even the Sunshine Coast are all over capacity according to the report. .

Meanwhile, Perth and Port Pirie are closer to their “ideal size.”

This tells us something important about urban growth: Australia’s population distribution is increasingly lopsided.

Some cities are bursting at the seams, while others aren’t reaching their potential.

What needs to change?

Associate Professor Liton Kamruzzaman, who led the study, suggests practical solutions:

Smarter transport links to reduce congestion,

Better balance of jobs across regions (not just clustered in one CBD),

Fairer land-use rules that encourage sustainable development.

In other words, we need policies that don’t just encourage growth but also manage it.

If we get it right, we can build cities that are big enough to thrive, but not so big that they collapse under their own weight.

What it means for property investors

For property investors, the Gold Coast remains a market underpinned by strong demand and limited supply; a combination that usually pushes prices higher.

With the Olympics on the horizon, infrastructure investment underway, and interstate migration still flowing, it’s hard to see demand easing anytime soon.

But affordability pressures, rental stress, and liveability challenges are flashing red lights.

Investors are likely to find better investment options in Brisbane where significant growth potential remains, without the same structural pressures.

But, as always, will need to be selective, focusing on locations that benefit most from infrastructure upgrades and lifestyle demand.

If you’re like many property investors, you’re probably wondering what’s the right thing to do at present.

Should you buy, should you sell, or should you just wait?

You can trust the team at Metropole to provide you with direction, guidance, and results.

Whether you’re a beginner or an experienced investor, at times like we are currently experiencing you need an advisor who takes a holistic approach to your wealth creation and that’s exactly what you get from the multi-award-winning team at Metropole.

We help our clients grow, protect and pass on their wealth through a range of services including:

Strategic property advice – Allow us to build a Strategic Property Plan for you and your family. Planning is bringing the future into the present so you can do something about it now! Click here to learn more

Buyer’s agency – As Australia’s most trusted buyers’ agents we’ve been involved in over $4Billion worth of transactions creating wealth for our clients and we can do the same for you. Our on the ground teams in Melbourne, Sydney, and Brisbane bring you years of experience and perspective – that’s something money just can’t buy. We’ll help you find your next home or an investment-grade property. Click here to learn how we can help you.

Property Development – We enable you to become an “armchair developer” and get all the benefits of property development without getting your hands dirty. We take the hassles out of your investment by assisting you with all the expertise you need, from concept to completion, including construction. Click here to see if it’s the right way for you to grow your portfolio.

Property Management – Our stress-free property management services help you maximise your property returns. Click here to find out why our clients enjoy a vacancy rate considerably below the market average, our tenants stay an average of 3 years, and our properties lease 10 days faster than the market average.

About Brett Warren Brett Warren is National Director of Metropole Properties and uses his two decades of property investment experience to advise clients how to grow, protect and pass on their wealth through strategic property advice.

The biggest fortunes in property are created before the main boom, when smart investors act while others hesitate.

It’s about positioning early, not chasing growth once it’s obvious.

We’re entering a period of prolonged property price growth, not necessarily a short-lived boom.

Despite negative headlines around affordability, productivity, and the economy, opportunities are emerging now.

Over the last 50 years in property, I’ve seen this play out time and time again…

The real fortunes in property aren’t made during the boom.

They’re made before the main property boom by investors who recognise the signs, trust the process, and have the courage to act while everyone else is sitting on their hands.

Right now, we’re at the beginning of a new property Super Cycle. I’m not suggesting this will be a boom, but a period of prolonged property price growth.

It might not feel like it – there’s still a lot of noise, headlines about Australia’s economic problems, affordability issues, productivity issues, and a heap of mixed economic messages.

But experienced investors know… this is when the real opportunities emerge.

Looking back, I’ve noticed something interesting.

The most successful property investors didn’t just work hard, or time the market perfectly, or get every decision right.

They got lucky—and they were ready to take advantage of it.

Now, luck in property might look like stumbling across the right property at the right price, meeting the right advisor at the right time, or having the discipline to hold onto an asset others were too nervous to buy.

But that’s not the luck that made them wealthy.

It was their ability to see the opportunity and take action—even when others were hesitating.

I’ve watched this unfold at the start of every property cycle.

Some investors wait and worry… others prepare and pounce.

Guess which group ends up looking like geniuses five years later?

So here’s the mindset shift: Don’t wait for perfect conditions—they don’t exist. Get clarity. Get a strategy. Get in position.

Because the new cycle has already begun earlier this year when interest rates started to fall, and this is exactly when the next generation of property millionaires quietly start building their wealth.

Now’s the time to get ready for your next move.

And if you’re unsure where to begin—or want a second opinion on your strategy – why not organise a complimentary Wealth Discovery Chat with our team at Metropole?

We’ll help you cut through the noise, identify your opportunities, and create a personalised plan to build lasting wealth—safely and strategically.

Click here and lock in a time for your chat with a Metropole Wealth Strategist

Remember: the luck will come.

The real question is… will you be ready to act on it?

About Michael Yardney Michael is the founder of Metropole Property Strategists who help their clients grow, protect and pass on their wealth through independent, unbiased property advice and advocacy. He’s once again been voted Australia’s leading property investment adviser and one of Australia’s 50 most influential Thought Leaders. His opinions are regularly featured in the media.

Middle-ring suburbs are evolving due to state-led rezoning, medium/high-density housing, and the rise of 20-minute neighbourhoods.

These changes aim to reduce urban sprawl, increase housing supply, and make better use of existing infrastructure.

Whether you own a home, hold apartments, or are eyeing development sites, Australia’s middle-ring transformation is creating new upside.

Rather than seeing urban transformation as a threat, it’s a once-in-a-generation opportunity.

Australia’s middle-ring suburbs are undergoing a significant transformation, driven by a combination of state-led rezoning initiatives, the introduction of medium- and high-density developments, and a strategic shift towards creating “20-minute neighbourhoods.”

This evolution presents both opportunities and challenges for existing homeowners and investors.

Embracing the ‘missing middle’ in urban planning

The term “missing middle” refers to the lack of medium-density housing options, such as townhouses, duplexes, and low-rise apartments, that bridge the gap between single-family homes and high-rise towers.

Historically, Australia’s housing landscape has been characterised by either low-density outer suburban sprawl or large-scale apartment blocks in urban cores, resulting in a stark divide in housing availability and affordability.

To correct this imbalance, various state governments – particularly in New South Wales Victoria, and the ACT – are introducing planning reforms that encourage medium-density infill housing in established suburbs designed to unlock underutilised land near existing infrastructure, create more housing choice, and reduce urban sprawl.

However, not everyone is on board.

Local councils, under pressure from vocal constituents who don’t want their neighbourhood character to change, are often pushing back against these proposals.

These constituents – often labelled NIMBYs (Not In My Backyard) – fear increased traffic, parking shortages, loss of privacy, and changes to the “leafy” character of their streets.

In turn, councils are implementing height restrictions, design overlays, and delaying rezoning approvals in an effort to appease existing residents.

This tension between state government objectives and local council resistance continues to slow down the rollout of much-needed housing diversity across our middle-ring suburbs.

Nonetheless, the push for the missing middle is gaining traction, as the need for more housing and better land use intensifies, especially in suburbs well served by transportation and amenities.

The rise of 20-minute neighbourhoods

The concept of the 20-minute neighbourhood is central to contemporary urban planning strategies, particularly in Melbourne’s “Plan Melbourne 2017-2050.”

The idea is to create communities where residents can access most of their daily needs, such as shops, schools, parks, and public transport, within a 20-minute walk or cycle from their homes.

This approach promotes local living, reduces reliance on cars, and fosters healthier, more connected communities.

Pilot programs in suburbs like Strathmore, Croydon South, and Sunshine West have demonstrated the potential of this model to enhance liveability and sustainability.

Implications for property owners

1. Increased Land Value Through Rezoning

Properties located near transport hubs or shopping strips that are rezoned for higher density will experience significant value appreciation.

Developers often seek to amalgamate such sites for larger projects, offering premiums to current owners.

2. Enhanced Local Amenities and Gentrification**

New developments often bring improved infrastructure, retail outlets, and public spaces.

This influx will revitalise neighbourhoods, making them more attractive to a diverse demographic, thereby increasing demand and property values.

3. Rising Demand for Established Apartments

With construction costs escalating, new apartments are entering the market at higher price points.

This scenario makes well-maintained existing family friendly apartments more appealing due to their relative affordability, potentially boosting their market value.

Challenges to consider

There is no doubt that the middle ring suburbs of our capital cities will look very different over the next decade, and while this will bring many benefits, there will also be challenges.

1. Potential Oversupply in Certain Areas

Rapid development can lead to an oversupply of apartments in specific locales, potentially stabilising or even reducing prices in the short term.

We saw this during the property construction group of 2014 – 17, when some locations just had too much speculative development.

While it’s likely new apartment development will roll out more slowly this time round, investors should monitor local development pipelines and vacancy rates to make informed decisions.

2. Impact on Low-Density Residences

Homes adjacent to new high-density projects might experience increased traffic, noise, and reduced privacy.

However, properties slightly removed from these developments will benefit from improved amenities without the immediate drawbacks.

3. Necessity for Property Upgrades

To remain competitive, owners of older apartments will need to consider renovations to match the appeal of newer constructions.

There’s nothing new about this – modernising interiors and amenities enhances rental yields, gives you a wide selection of potential tenants and improves the value of your property.

A golden opportunity for strategic investors

While some homeowners may worry about the changes medium- and high-density developments bring to their suburbs, strategic property investors see the bigger picture, and it’s full of upside.

Rezoning in middle-ring suburbs is creating significant opportunities.

Properties close to transport hubs and vibrant local centres are becoming development hotspots.

As land becomes more valuable, savvy investors are acting decisively, unlocking the potential of these areas by buying older homes on sizeable blocks and building two townhouses where there was once just an old home.

But here’s the key difference: they’re not doing it to flip for short-term profit – they are holding onto these new townhouses as part of a long-term “build-to-hold” strategy.

This approach allows them to manufacture equity through development while also benefiting from growing rental yields, long-term capital growth, and depreciation benefits.

And because many of these projects are in gentrifying suburbs with improved amenity, growing populations, and increased demand for quality housing, the long-term upside is incredibly compelling.

This is exactly the sort of strategy Metropole has specialised in for decades- guiding clients from property selection, through development feasibility, planning approvals, and construction, all the way to managing the end investment.

We’re not in the business of selling properties – we’re in the business of helping our clients build lasting wealth.

In this new phase of urban transformation, where the ‘missing middle’ is finally being built and the 20-minute neighbourhood becomes a reality, the investors who understand the power of location, timing, and strategic development will be the ones who benefit most.

Even if you’re not sitting on a development site, these changes are driving more people into previously overlooked suburbs, breathing new life into local economies and increasing demand for well-located established properties.

And with construction costs still high, the price gap between new and existing apartments will remain wide, pulling the value of quality older stock upwards.

In short, Australia’s urban evolution isn’t a threat—it’s an invitation.

For those who understand the trends and invest with strategy, the next wave of growth will come not from chasing hotspots, but from riding the structural shifts reshaping our cities.

So rather than resisting the changes sweeping through our suburbs, the question investors should be asking is: how can I ride this wave of transformation to build intergenerational wealth.

About Michael Yardney Michael is the founder of Metropole Property Strategists who help their clients grow, protect and pass on their wealth through independent, unbiased property advice and advocacy. He’s once again been voted Australia’s leading property investment adviser and one of Australia’s 50 most influential Thought Leaders. His opinions are regularly featured in the media.

Let’s be honest—playing the lottery feels like harmless fun. A couple of bucks for a shot at financial freedom, right?

But here’s the problem: it’s not harmless when people actually believe it’s a strategy to build wealth.

It’s not. It never was. In fact, I’d argue that playing the lottery is just a tax on people who don’t understand maths.

As someone who’s spent decades teaching Australians how to achieve financial independence through property and smart money habits, it pains me to see people throw away their dreams chasing scratchies and Powerball fantasies.

Tip: Believe it or not…You’re more likely to be crushed by a vending machine than win the lotto!

So let’s have a bit of fun and reality-check this.

The Odds Are Wildly Against You

You know the odds of winning the Powerball jackpot in Australia? 1 in 134,490,400.

Let me repeat that. One in 134 million.

You are literally more likely to do just about anything else in life—including some things that sound like plot points in a bad movie—than win the lottery.

Here Are 20 Things That Are More Likely Than Winning the Lottery

Being struck by lightning – Odds are about 1 in 1.6 million in your lifetime. It’s rare—but still nearly 100 times more likely than winning Powerball.

Becoming a billionaire – According to Forbes, your odds are about 1 in 409,000. You’re over 300 times more likely to become a billionaire than win the lottery.

Dying in a plane crash – About 1 in 11 million. Still more likely than winning.

Getting attacked by a shark in Australia – Around 1 in 3.7 million. (So yes, go ahead and swim at Bondi, you’ve still got a better shot than winning lotto.)

Crushed by a vending machine – Around 1 in 112 million. Silly? Sure. But still a higher probability.

Becoming a movie star – The odds? About 1 in 1.5 million. In other words, Hollywood is more accessible than your dream lotto lifestyle.

Bowling a perfect 300 game – About 1 in 11,500 for regular league bowlers.

Becoming an astronaut – NASA accepts about 1 in 12,000 applicants. Start training!

Dating a supermodel – Depending on how you define it (and your charm), studies suggest it’s around 1 in 88,000.

Being dealt a royal flush in poker – 1 in 649,740. Vegas is calling.

Having identical quadruplets – About 1 in 15 million. Not impossible.

Writing a New York Times bestseller – About 1 in 220,000 if you finish your book. Better odds than lotto!

Finding a four-leaf clover on your first try – 1 in 10,000.

Becoming Prime Minister of Australia – Around 1 in 8.9 million. Even that’s more achievable.

Getting hit by a meteorite – 1 in 74 million.

Winning an Olympic gold medal – 1 in 662,000 (if you train full-time from a young age).

Solving a Rubik’s Cube blindfolded – 1 in 50 for serious cubers. Still easier than picking the winning numbers.

Becoming a professional AFL player – Roughly 1 in 89,000.

Being born with 11 fingers or toes – Happens to about 1 in 500 babies. No ticket required!

Living past 100 – Around 1 in 5,000. Better start eating your veggies.

But Michael, What If I Win?

Yes, someone eventually does win. That’s how the system keeps running.

But here’s the catch: most lottery winners lose their money anyway.

A 2010 study from the National Endowment for Financial Education in the US found that 70% of people who suddenly receive a windfall – like lottery winners- lose it within a few years.

Why?

Because money doesn’t make you financially free. Financial literacy, discipline, and smart investing do.

What You Should Be Doing Instead

If you’re hoping for a better financial future, don’t rely on a system designed to take your money.

Instead:

Educate yourself about finance and the psychology of money

Invest in assets that grow in value (like residential property)

Surround yourself with good advisors, not lucky tickets

So, Is the Lottery Really Just a Tax?

Yes. And here’s the kicker: it’s a tax on those who can least afford it.

Lower-income earners are statistically more likely to buy lotto tickets, hoping for a miracle. That’s heartbreaking.

But wealth isn’t built on miracles. It’s built on mindset, strategy, and time.

Final Thoughts

There’s nothing wrong with a bit of fun.

If you want to throw a few bucks at a Powerball ticket every now and then, go for it. Just treat it as entertainment, not a wealth plan.

But if you’re serious about becoming financially independent, forget the lotto. It’s time to stop hoping—and start planning.

Because while you may never win the lottery, you can absolutely build a life that feels like you did.

About Michael Yardney Michael is the founder of Metropole Property Strategists who help their clients grow, protect and pass on their wealth through independent, unbiased property advice and advocacy. He’s once again been voted Australia’s leading property investment adviser and one of Australia’s 50 most influential Thought Leaders. His opinions are regularly featured in the media.

Many predictions about real estate markets and property prices are just educated guesses or misleading information.

Rather than trying to time the market, investors should adopt a long-term perspective for their property investment.

There is no “best” time or “worst” time to buy property because property investment is a process, not just an event.

Attempting to time the market could lead to missed opportunities, and waiting for the “perfect” moment to invest may result in a more competitive market and potentially higher prices.

Planning is crucial for property investment, and a well-executed plan can help investors achieve their financial goals and maximise their wealth creation through property.

A Strategic Property Plan should contain several components, including an asset accumulation strategy, a manufacturing capital growth strategy, a rental growth strategy, an asset protection and tax minimisation strategy, a finance strategy, and a living off your property portfolio strategy.

I don’t know about you, but I’m seeing a lot of so-called “experts” on social media confidently forecasting the direction of our real estate markets and property prices for the balance of 2025 and well into next year.

However, if they really knew how to predict our markets, these individuals would likely be enjoying a luxurious lifestyle, reaping the rewards of their market insights.

The reality is that most predictions are, at best, educated guesses and, at worst, misleading information.

Now it’s not just the social media experts.

Just look at those failed predictions from bank economists, financial institutions and research houses over the last few years.

And what about the interest rate cliff or the unemployment cliff or all those other dire press that didn’t eventuate?

For instance, during the onset of the COVID-19 pandemic, some predicted a significant market downturn, which didn’t materialize.

Then many predicted price falls of 20 to 30% because of rising interest rates and that didn’t happen.

Sure we’ve just experienced a year of falling property prices when the interest rates started rising, but almost anyone who bought a well-located property over the last couple of years ago is sitting on some significant equity gains.

So what should an investor do?

For the majority of us mere mortal investors who don’t have a crystal ball, rather than trying to time the market it’s essential to adopt a long-term perspective for your property investment.

There is no “best” time or “worst” time to buy property because property investment is a process, not just an event.

So rather than just talking about going out and buying a property in 2025 or 2026, the right time for you to consider investing is when you have all your ducks in a row.

For some of you who are reading this right now will absolutely be the worst possible time you could consider buying a property.

For others there is a window of opportunity because it’s likely when looking back next year, many will recognise the the market boomed as falling inflation, increasing consumer confidence, lower interest rates, and first homeowner grants were a stunning combination that fuelled the flames of our housing market.

Many people who mistimed the last upswing missed out on profitable opportunities.

They are now cashed up and ready to buy and will hop into the market as the media changes its message.

This means attempting to time the market could lead to missed opportunities.

Investors who wait for the “perfect” moment to invest may find themselves competing with other buyers who return as the market slowly picks up.

Remember the fundamental economic principle of supply and demand?

If you wait for the market to “improve,” you’ll likely face a more competitive market, making it harder to find a quality property in a desirable location, and potentially at a higher price.

Isn’t it too early to get into the market?

Throughout the years, countless investors have regretted not purchasing high-quality properties earlier.

All the major research houses, are now suggesting significant property price growth over the next two years.

Here is what ANZ Bank forecasts for house prices:

These are Domain’s property price forecasts.

You need to plan

So while the property markets will create significant wealth for many Australians, statistics show that 50% of those who buy an investment property sell up in the first five years.

And of those who stay in the investment game, 92% never get past their first or second property.

That’s because attaining wealth doesn’t just happen, it’s the result of a well-executed plan.

Planning is bringing the future into the present so you can do something about it now!

Just to make things clear…buying an investment property is NOT a strategy!

It’s important to start with the end game in mind and understand what you need and what you want to achieve.

And then you have to build a plan, a strategy to get there.

The property you eventually buy will be the physical manifestation of a whole lot of decisions that you will make, and they must be made in the right order

That’s because property investment is a process, not an event.

If you’re a beginner looking for a time-tested property investment strategy or an established investor who’s stuck or maybe you just want an objective second opinion about your situation, I suggest you allow the team at Metropole to build you a personalised, customised Strategic Property Plan.

When you have a Strategic Property Plan you’re more likely to achieve the financial freedom you desire because we’ll help you:

Define your financial goals;

See whether your goals are realistic, especially for your timeline;

Measure your progress towards your goals – whether your property portfolio is working for you, or if you’re working for it;

Find ways to maximise your wealth creation through property;

Identify risks you hadn’t thought of.

And the real benefit is you’ll be able to grow your wealth through your property portfolio faster and more safely than the average investor.

Your Strategic Property Plan should contain the following components:

An asset accumulation strategy

A manufacturing capital growth strategy

A rental growth strategy

An asset protection and tax minimisation strategy

A finance strategy including long-term debt reduction and…

A living off your property portfolio strategy

Click here now and learn more about this service and discuss your options with us.

About Brett Warren Brett Warren is National Director of Metropole Properties and uses his two decades of property investment experience to advise clients how to grow, protect and pass on their wealth through strategic property advice.

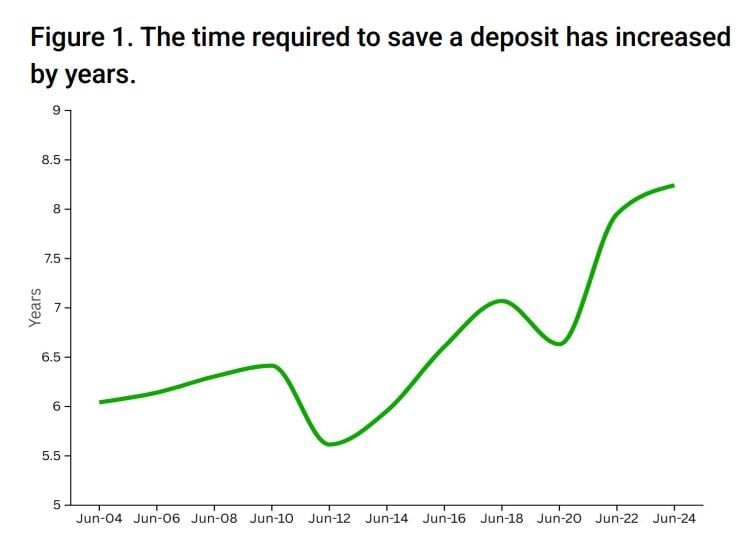

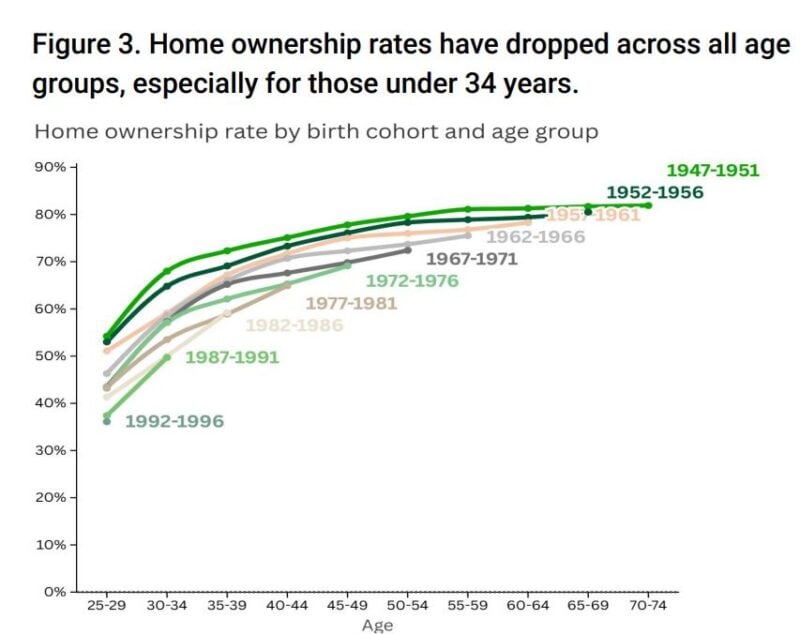

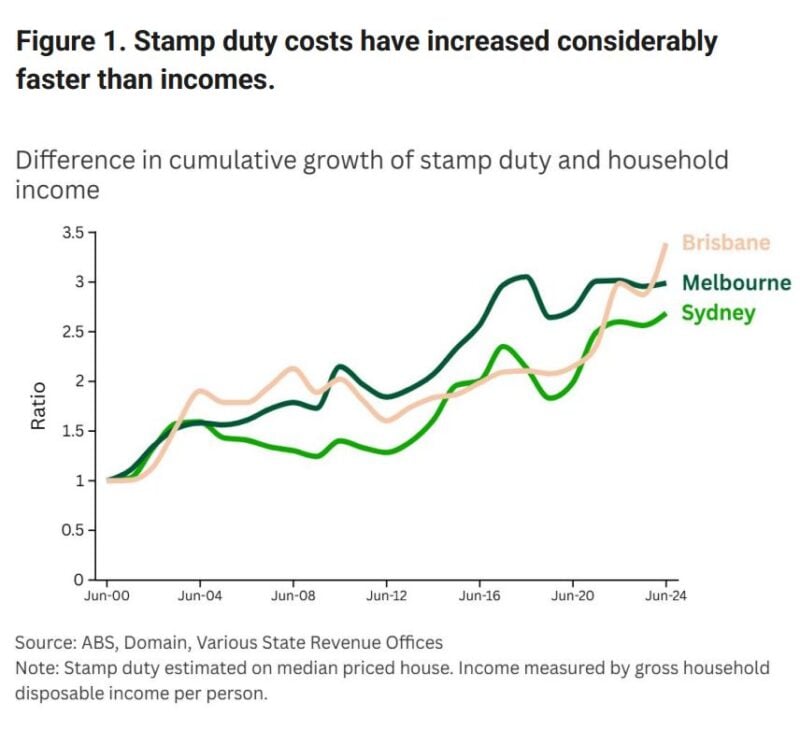

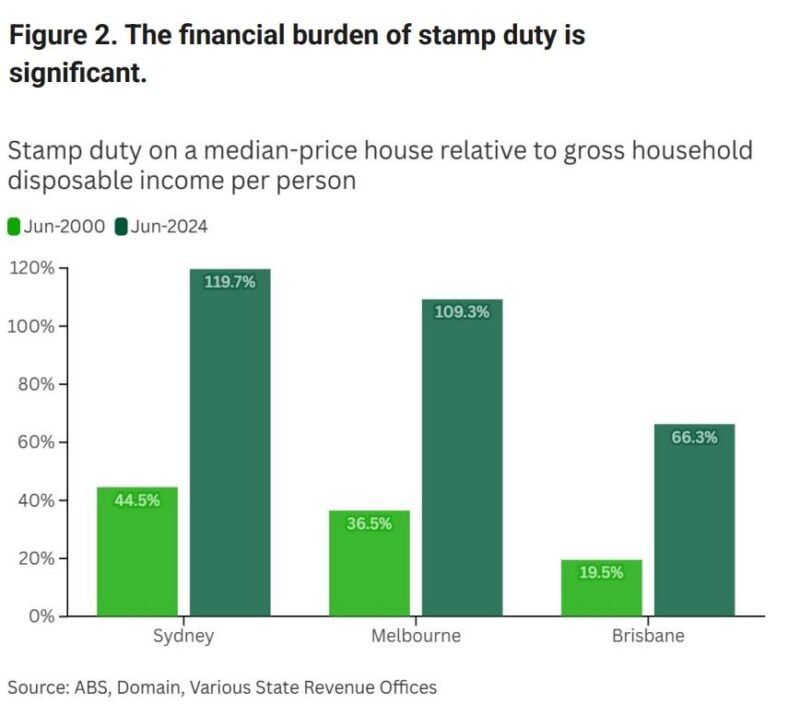

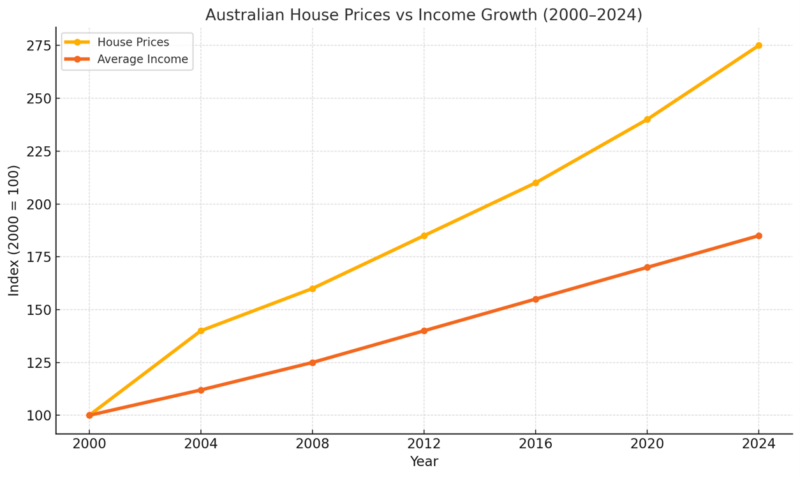

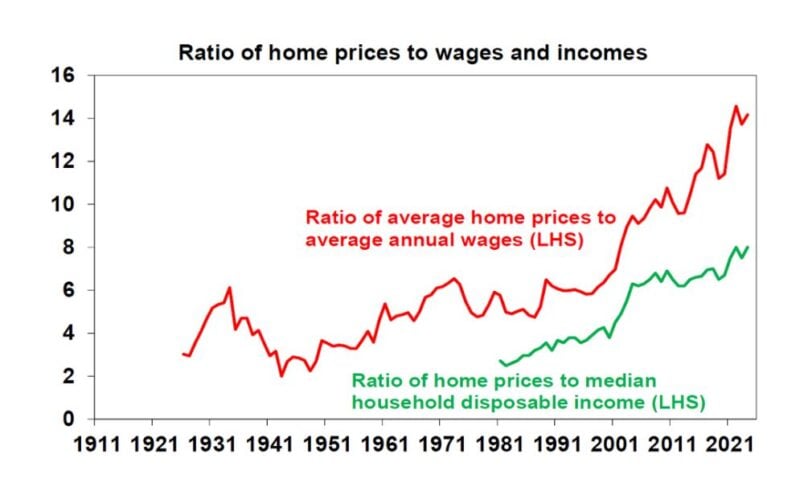

It now takes the median-income household over 8 years to save for a 20% deposit, compared to just 6 years in the early 2000s.

This “deposit gap” has become the single biggest hurdle for first-home buyers.

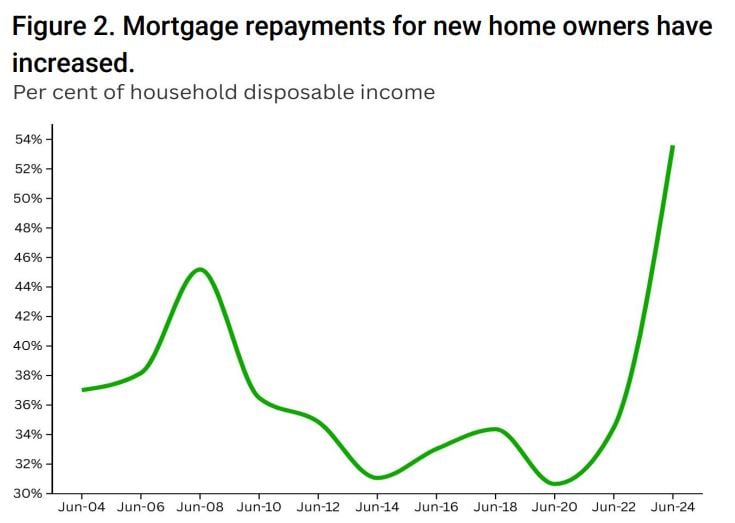

A typical new home loan consumes around 54% of household disposable income—the highest level in at least 20 years.

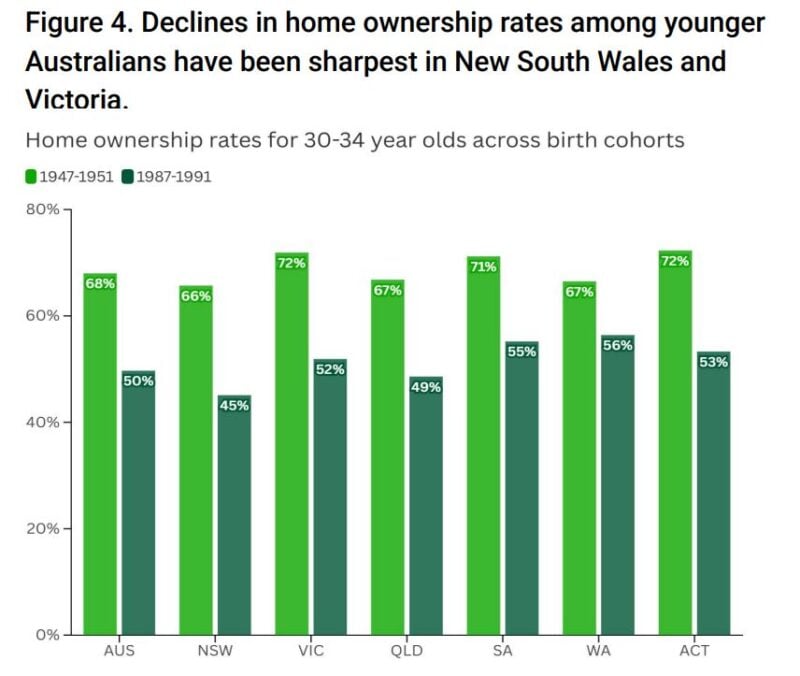

Home ownership rates for Australians under 34 have dropped sharply across every state, particularly in NSW and Victoria.

Those born in the late 1980s and early 1990s are significantly less likely to own a home compared to Baby Boomers, highlighting a structural intergenerational inequality.

The decline in young home ownership is not unique to Australia—it’s also seen in the UK, US, and Europe.

Contributing factors include insecure work, later marriage, and fewer children, which reduce the urgency or ability to buy a home.

Remember when owning a home was considered a rite of passage? A marker of stability and success?

Today, for many Australians, that milestone feels more like a distant fantasy than a realistic goal.

What was once seen as the cornerstone of financial security has become an uphill battle, with soaring property prices, stricter lending rules, and wages that simply haven’t kept pace.

Owning a home has always been the cornerstone of the Australian dream.

But for younger generations, that dream is slipping further out of reach.

“Affordable” homes are becoming unaffordable

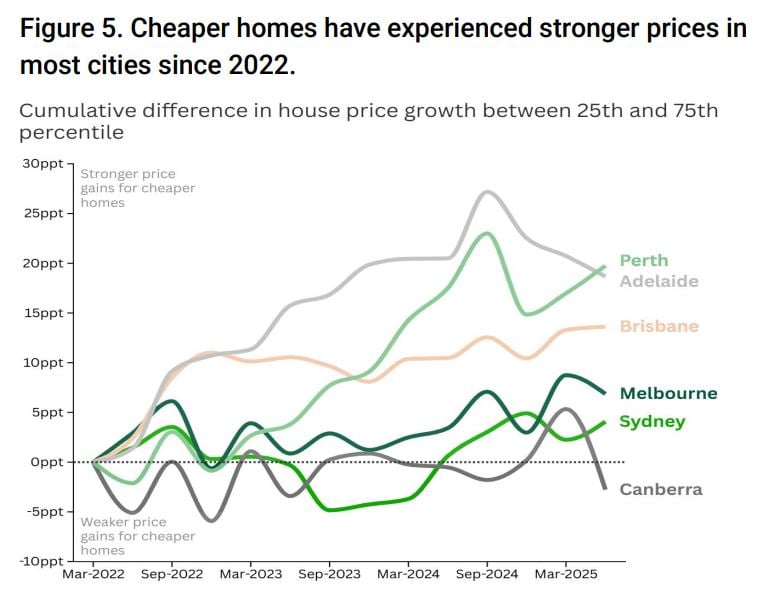

According to research by Domain, houses priced in the 25th percentile – typically purchased by first home buyers – have increased in price at a greater rate than premium houses (those in the 75th percentile) across most major capitals since 2022 – as the figures below show.

Cumulative difference in house price growth for entry-level homes compared with premium homes:

Sydney: 4.1 ppts

Melbourne: 6.9 ppts

Brisbane: 13.6 ppts

Adelaide: 18.7 ppts

Perth: 19.8 ppts

The deposit mountain

The biggest barrier for first-home buyers isn’t servicing the loan—it’s scraping together the deposit.

According to Domain, a median-income household now needs more than eight years to save for a 20% deposit, compared to just six years in the early 2000s.

Dr Nicola Powell, Domain’s Chief of Research and Economics, says this has reshaped the entry point into the market:

“The time it takes to save a deposit has blown out dramatically.

For many first-home buyers, it’s not the repayments that keep them out of the market, it’s the sheer challenge of getting a foothold with such a large upfront cost.”

Mortgage stress at record highs

Even once buyers leap the deposit hurdle, they face much tougher repayments.

A typical new loan now consumes around 54% of disposable household income, the highest level in more than 20 years.

This shift has been driven by the double blow of rapidly rising property prices and the sharp lift in interest rates after 2022.

While rate cuts in 2025 offered some relief, prices kept surging, offsetting much of the benefit.

Dr Powell notes:

“We’ve moved into a world where home ownership is becoming more exclusive.

Lower interest rates in recent years did help with repayments, but because prices rose even faster, the affordability equation actually worsened for many.”

A widening generational divide

The impact is starkest among younger Australians.

Home ownership rates for under-34s have dropped across every state, with the sharpest falls in New South Wales and Victoria.

Search trends reveal more Australians now looking for “dual”, “granny” and “duplex” properties, reflecting rising interest in higher-density and more affordable housing options.

What needs to change?

The affordability challenge is structural, not cyclical.

It’s not just about where interest rates sit today.

Barriers like stamp duty, restrictive lending standards, and surging deposit requirements are locking more people out each year.

Potential reforms flagged by Domain include:

Replacing stamp duty with a broad-based land tax, to reduce upfront costs and improve mobility.

Expanding shared-equity and low-deposit schemes, to bridge the deposit gap for first-home buyers.

Reviewing lending standards, to strike the right balance between stability and access to credit.

Dr Powell concludes:

“If we want to restore the Australian dream of home ownership, we need coordinated reform.

Without it, the divide between the housing haves and have-nots will only deepen.”

Final thoughts

The numbers are clear: affordability has reached breaking point.

For first-home buyers, the challenge isn’t just paying off a mortgage, it’s finding a way to even get in the game.

And unless structural reforms are made, home ownership risks becoming a privilege for the few, rather than the foundation of financial security it has long been in Australia.

About Brett Warren Brett Warren is National Director of Metropole Properties and uses his two decades of property investment experience to advise clients how to grow, protect and pass on their wealth through strategic property advice.

Australians rarely talk openly about money, yet most wonder: “Am I doing okay financially?”

Comparing across generations reveals both challenges and opportunities.

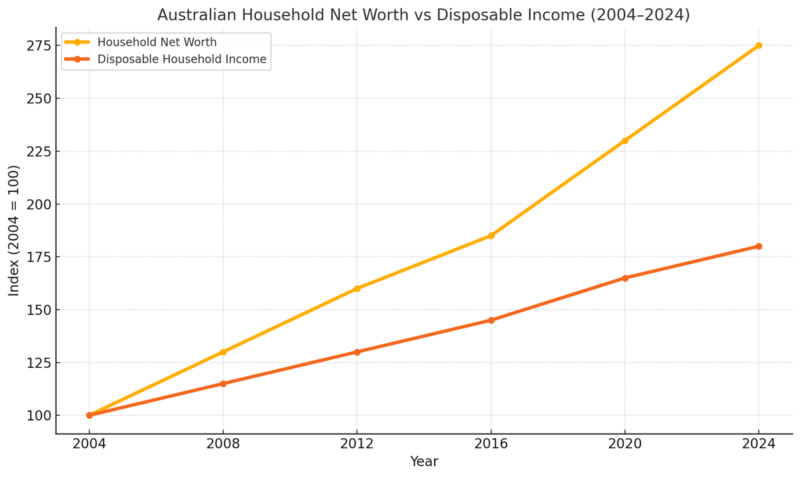

Once a large “middle,” Australia’s wealth distribution now looks more like a U-shape.

Many households are either asset-rich or asset-poor, with fewer in between.

Policy shifts increasingly target the top and bottom, leaving the middle less influential.

It’s human nature to compare.

We compare homes, cars, holidays, and yes, we compare wealth.

But most Australians don’t talk openly about money, so it’s hard to know where we really stand.

Have you ever caught yourself thinking: “Am I doing okay financially?”

Whether you’re a Baby Boomer enjoying retirement, a Gen Xer in your prime earning years, a Millennial juggling work and family, or a Gen Z just starting out, it’s only natural to want to know how you stack up.

So in this episode of Demographics Decoded, leading demographer Simon Kuestenmacher and I take a closer look at the wealth profiles of each generation in Australia.

The numbers may surprise you, but more importantly, the lessons they reveal can help you chart your own financial future.

For weekly insights subscribe to the Demographics Decoded podcast, where we will continue to explore these trends and their implications in greater detail.

Subscribe now on your favourite Podcast player:

The disappearing middle

Once upon a time, we thought of Australia as a land of three clear groups: the rich, the poor, and a big, stable middle class.

But as Simon Kuestenmacher explains in our latest episode of Demographics Decoded, that’s no longer the case:

“Instead of the old bell curve of wealth with a big bulge in the middle, today we see a U-shape. There are plenty of households with relatively low wealth, plenty with high wealth, but fewer in between.”

That shrinking middle has real consequences.

In the past, governments could design policies for “the middle class” and reach most Australians.

Today, policies tend to tilt either to the lower-income or higher-income groups.

The middle doesn’t carry the same weight it once did.

Baby Boomers: the asset-rich generation (born 1946–1964)

Boomers have had time on their side.

They bought homes when property prices were modest relative to incomes, benefited from decades of growth, and have ridden the long bull run in property and shares.

On average, boomer households today hold:

$1.3 million in property assets

$641,000 in superannuation or business assets

$206,000 in shares

$240,000 in cash savings

That totals around $2.3 million in net wealth, with relatively little debt (about $82,000).

Boomers hold roughly half of Australia’s housing wealth, much of which will flow to younger generations in the coming decades.

As Simon reminds us:

“We’re heading into a once-in-a-lifetime wealth transfer. In the next 10 to 15 years, somewhere between $3 and $6 trillion will shift from boomers to their children, mostly millennials. But not every millennial will inherit, so the divide between those who do and those who don’t will widen further.”

Gen X: the sandwich generation (born 1965–1980)

If you’re a Gen Xer, you’re probably in your 40s or 50s, earning well, but also carrying some heavy financial burdens.

Gen X households average:

$1.3 million in property assets

$586,000 in superannuation

$256,000 in shares

$176,000 in cash

That equates to $1.88 million net wealth, but with close to $450,000 in debt.

They’re called the “sandwich generation” for a reason.

Many are still supporting kids at home (often into their 20s), while also helping ageing parents.

Add in big mortgages taken on during the pandemic’s ultra-low interest rate period, and Gen X feels the squeeze.

Simon points out the risks:

“This is the cohort banks are most worried about. They borrowed heavily during the boom, and now, with higher rates, some jobs at risk of automation, and households relying on two incomes, it could become fragile.”

Yet the future looks brighter. Within a decade, many of these pressures will lift.

Children will move out, mortgages will be paid off, and parents will pass on inheritances.

Gen X may move from stress to surplus almost overnight.

Millennials: playing catch-up (born 1981–1996)

Millennials are often the most frustrated generation.

They’ve worked hard, studied harder, and many are raising families, yet feel locked out of the financial security their boomer parents enjoyed.

Their averages:

$750,000 in property

$260,000 in superannuation

$51,000 in shares

$104,000 in cash

That gives them a net wealth of about $757,000, well below Gen X and boomers.

Millennials make up 15% of households, but hold only 5% of Australia’s wealth.

It’s not hard to see why they’re frustrated.

Property is far more expensive relative to incomes than it was for their parents.

University, once a ticket to a secure and high-paying job, now often comes with years of debt.

As Simon explains:

“Millennials compare themselves to their boomer parents and feel left out. Their parents could buy a house on a single income. Today, you need two incomes and still stretch to the limit. So millennials look for alternatives: ETFs, shares, even crypto.”

But that search for shortcuts comes with risk.

“Most millennials holding crypto are what I call ‘squiggly line investors’ – hoping a few thousand dollars will magically turn into millions. A few got lucky with Bitcoin, but it’s speculation, not strategy.”

The positive? Millennials still have decades ahead to grow wealth the traditional way, step by step, year by year, through disciplined investing.

Gen Z: just getting started (born 1997–2012)

Gen Z is only just entering the workforce, yet already has an average net wealth of $96,000, largely thanks to compulsory super contributions, which start accumulating even in teenage jobs.

But they also carry around $49,000 in debt, mostly student-related.

As Simon notes:

“It’s too early to judge. They’re still at the starting line. Their challenge will be getting onto the property ladder, which is tougher than ever.”

Many will look to alternative investments, but as always, the fundamentals of wealth creation remain the same: spend less than you earn, invest wisely, and give it time.

The bigger picture

So what can we learn from all this?

Averages hide as much as they reveal. You’re not your generation’s average. Some will be far ahead, while others will be far behind. Don’t fall into the comparison trap.

Wealth takes decades to build. Baby Boomers didn’t get rich overnight; they accumulated wealth steadily. Millennials and Gen Z can too.

Lifestyle inflation is the real enemy. More income is meaningless if you simply spend more.

Property remains Australia’s cornerstone of wealth. Our residential property market is valued at around $11.4 trillion, with debt totalling just $2.4 trillion. That’s why real estate, combined with superannuation, continues to underpin household net worth.

And as Simon wisely says:

“Don’t be discouraged. The key is to be deliberate and strategic – in how you earn, spend, and invest. That’s what’s in your control.”

Final thoughts

If you’re ahead of the averages, well done.

Just remember: preserving wealth is as important as creating it.

If you’re behind, don’t panic.

The best time to start was 20 years ago. The second-best time is today.

At Metropole, we help Australians of all generations build, protect, and pass on their wealth safely and strategically.

With the right plan, you can set yourself up not just to “stack up” against your generation, but to move ahead of the curve.

If you found this discussion helpful, don’t forget to subscribe to our podcast and share it with others who might benefit.

Subscribe now on your favourite Podcast player:

About Michael Yardney Michael is the founder of Metropole Property Strategists who help their clients grow, protect and pass on their wealth through independent, unbiased property advice and advocacy. He’s once again been voted Australia’s leading property investment adviser and one of Australia’s 50 most influential Thought Leaders. His opinions are regularly featured in the media.

It is constantly taking in sensory data and information that is below the radar of the conscious mind.

As a result, it knows things the conscious mind does not.

It exists to not only help you survive but also to thrive.

You need to listen to your gut.

Those who do find luck.

About Tom Corley Tom is a CPA, CFP and heads one of the top financial firms in New Jersey. For 5 years, Tom observed and documented the daily activities of wealthy people and people living in poverty and his research he identified over 200 daily activities that separated the “haves” from the “have nots” which culminated in his #1 bestselling book, Rich Habits – The Daily Success Habits of Wealthy Individuals.

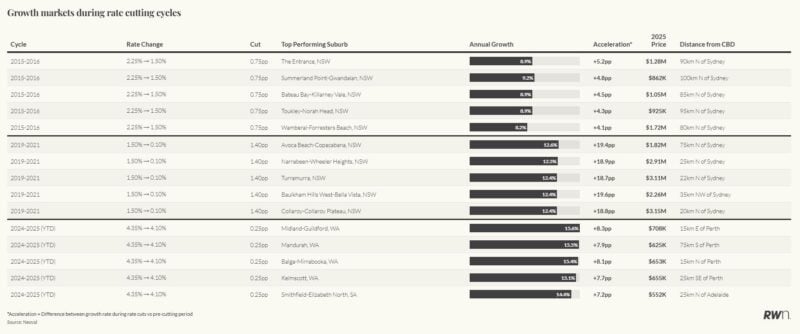

Each round of rate cuts since 2015 has benefited entirely different segments of the housing market, depending on affordability, demographics, and economic conditions.

Rate cuts alone don’t guarantee growth everywhere. The winners shift based on affordability, stimulus, and buyer profiles.

Smart investors look beyond history and focus on who stands to gain in the current environment.

If there’s one thing property investors learn over time, it’s that no two cycles are ever the same.

The past decade has reminded us of this lesson again and again.

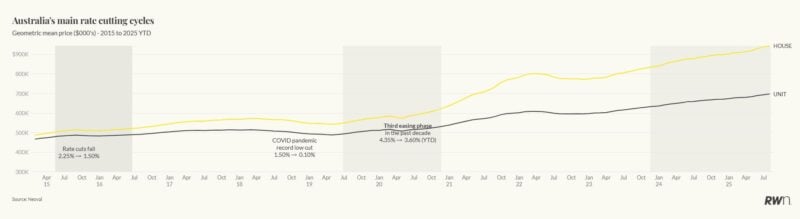

Since 2015, Australia has been through three major interest rate cutting cycles.

Each of these has played out very differently, with entirely different market segments benefiting depending on the broader economic backdrop and who was active in the market at the time.

And the way buyers respond to interest rate cuts is shaped just as much by affordability and demographics as it is by the cost of money itself.

Let’s take a look at a recent report by Nerida Conisbee explaining how these cycles unfolded—and more importantly, what lessons we can draw for the future.

The First Cycle (2015–2016): coastal lifestyle markets rise

When the RBA eased rates from 2.25% down to 1.50% between May 2015 and May 2016, the biggest winners weren’t blue-chip suburbs but affordable coastal lifestyle locations close to Sydney.

The Central Coast was the standout, with Avoca Beach–Copacabana (8.0%), Wamberal–Forresters Beach (8.2%), and The Entrance (8.9%) all showing strong growth.

Conisbee explains:

“This was when the lifestyle shift really began.

People were seeking coastal living within commuting distance, and cheaper borrowing costs made that possible well before COVID accelerated the trend.”

These markets, priced between $800,000 and $1.2 million at the time, highlight how rate cuts can amplify emerging lifestyle preferences.

The Second Cycle (2019–2021): premium Sydney suburbs surge

The next phase was far more aggressive according to Conisbee.

From mid-2019 through the pandemic, rates plunged from 1.50% to just 0.10%.

This time, the response was concentrated in Sydney’s premium suburbs.

Castle Hill, Baulkham Hills West–Bella Vista, and Northern Beaches areas like Collaroy and Freshwater all recorded double-digit growth.

Baulkham Hills West–Bella Vista alone swung from -7.2% to +12.4% growth, a 19.6 percentage point acceleration.

According to Conisbee:

“Ultra-low rates and fiscal stimulus created a pronounced wealth effect.

Established property owners, particularly in Sydney’s premium markets, were able to upgrade or expand their portfolios.

It wasn’t first home buyers driving this cycle, it was the affluent.”

This was a clear reminder that rate cuts don’t always make property more accessible, they can just as easily amplify demand where wealth is already concentrated.

The Third Cycle (2024–2025): affordable outer suburbs take the lead

Fast forward to today, and we’re in another cutting cycle; this time from the highest interest rates seen in over a decade.

But instead of boosting premium markets, affordability has become the driving factor.

Perth’s Midland–Guildford (15.6%), Mandurah (15.5%), and Balga–Mirrabooka (15.4%) are leading national growth.

In Adelaide, Smithfield–Elizabeth North is up 14.4%.

These are outer suburban markets priced between $550,000 and $750,000—very much first home buyer territory.

Conisbee notes:

“Unlike the COVID cycle, today’s cuts are most effective for buyers on the margins of borrowing capacity.

Affordable outer suburbs are where interest rate reductions translate directly into stronger demand.”

In other words, the affordability crisis has fundamentally reshaped who benefits when monetary policy loosens.

The consistent performers

While the beneficiaries have shifted from lifestyle seekers, to wealthy upgraders, to first home buyers, some regions have shown enduring sensitivity to rate cuts.

Conisbee highlights:

“The Central Coast is fascinating. Across all three cycles, it’s shown consistent growth.

That tells us some markets retain a structural advantage, whether that’s lifestyle appeal, location, or ongoing affordability relative to Sydney.”

Key lessons for investors

What should investors take away from this decade-long story?

Each cycle has its own winners. As Conisbee says, “We can’t assume that because one group benefited in the past, they’ll benefit again.”

Affordability now matters more than ever. Today’s rate-sensitive suburbs are not the million-dollar enclaves, they’re the $550k to $750k markets.

Some markets have lasting resilience. Places like the Central Coast show that structural appeal can cut across multiple cycles.

Context is everything. Fiscal stimulus, global shocks like COVID, and demographic shifts shape how rate cuts flow through the market.

Final thoughts – a new window of opportunity

The past decade of rate cycles proves just how dynamic and unpredictable Australia’s property market really is.

Conisbee sums it up well:

“Every cycle is different.

The beneficiaries shift depending on affordability, economic conditions, and who’s active in the market.

Understanding that context is critical for investors.”

As we look ahead, it’s clear that today’s easing is delivering the greatest benefits to outer suburban, affordable markets.

That’s a profound shift from the wealth-driven gains of the COVID cycle, and a reminder that strategy, not just timing, is what separates smart investors from the rest.

However, one thing is clear: there’s currently a window of opportunity for property investors with a long-term focus.

Right now, we’re seeing what some would call a “perfect storm” of fundamentals that are aligning to support strong property markets in the years ahead:

Continued rapid population growth is putting pressure on housing.

An acute undersupply of dwellings,

A chronic shortage of skilled labour, making new development slower and more expensive.

Inflation has moderated, now sitting within the RBA’s target range.

Interest rates will keep falling – bringing more buyers into the market

Government first homebuyer incentives will pour fuel on the flames of our undersupplied housing market.

As interest rates keep falling and confidence returns among both buyers and sellers, we’ll enter the next phase of the property cycle.

And historically, this stage has delivered some of the best capital growth for those who act early.

Are you clear on how to take advantage of these market conditions — or are you still waiting for “certainty”?

If you’re like many property investors, you’re probably wondering what’s the right thing to do at present.

Should you buy, should you sell, or should you just wait?

You can trust the team at Metropole to provide you with direction, guidance, and results.

Whether you’re a beginner or an experienced investor, at times like we are currently experiencing you need an advisor who takes a holistic approach to your wealth creation and that’s exactly what you get from the multi-award-winning team at Metropole.

We help our clients grow, protect and pass on their wealth through a range of services including:

Strategic property advice – Allow us to build a Strategic Property Plan for you and your family. Planning is bringing the future into the present so you can do something about it now! Click here to learn more

Buyer’s agency – As Australia’s most trusted buyers’ agents we’ve been involved in over $4Billion worth of transactions creating wealth for our clients and we can do the same for you. Our on the ground teams in Melbourne, Sydney, and Brisbane bring you years of experience and perspective – that’s something money just can’t buy. We’ll help you find your next home or an investment-grade property. Click here to learn how we can help you.

Property Development – We enable you to become an “armchair developer” and get all the benefits of property development without getting your hands dirty. We take the hassles out of your investment by assisting you with all the expertise you need, from concept to completion, including construction. Click here to see if it’s the right way for you to grow your portfolio.

Property Management – Our stress-free property management services help you maximise your property returns. Click here to find out why our clients enjoy a vacancy rate considerably below the market average, our tenants stay an average of 3 years, and our properties lease 10 days faster than the market average.

About Brett Warren Brett Warren is National Director of Metropole Properties and uses his two decades of property investment experience to advise clients how to grow, protect and pass on their wealth through strategic property advice.

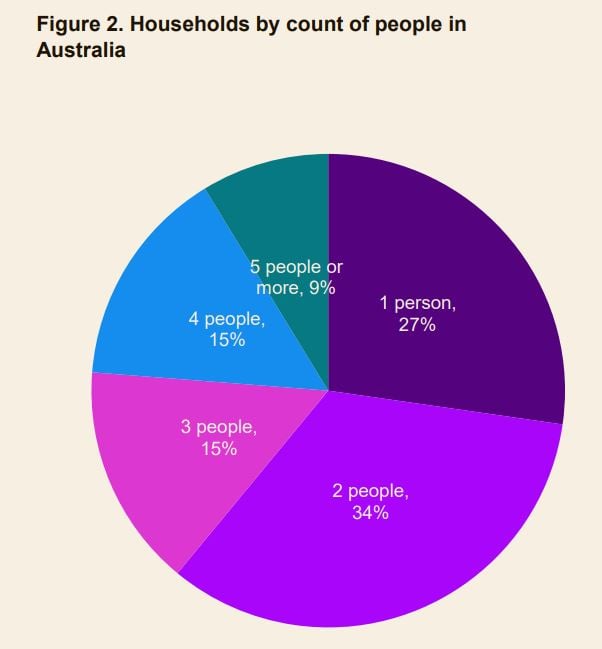

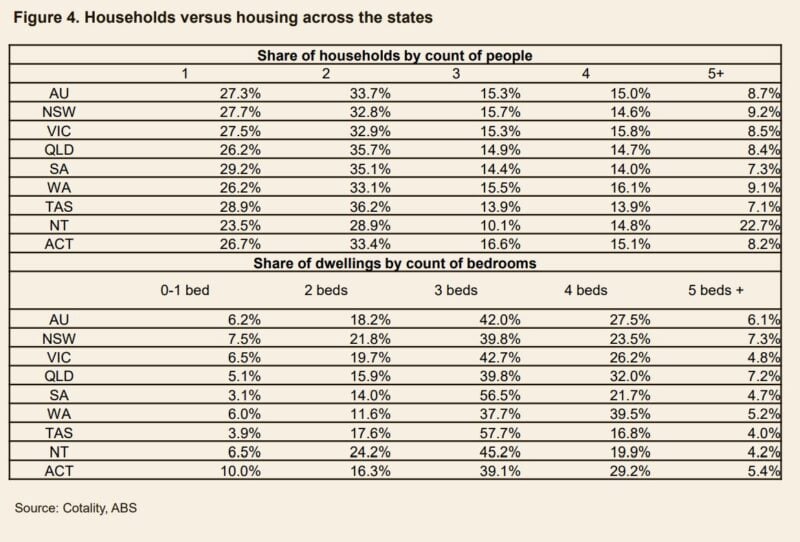

Single-person households are the fastest-growing household type in Australia.

This isn’t a short-term shift but a long-term demographic trend reshaping the housing market, economy, and community design.

Smaller households increase housing demand, not reduce it, because one person needs almost as much infrastructure as a family.

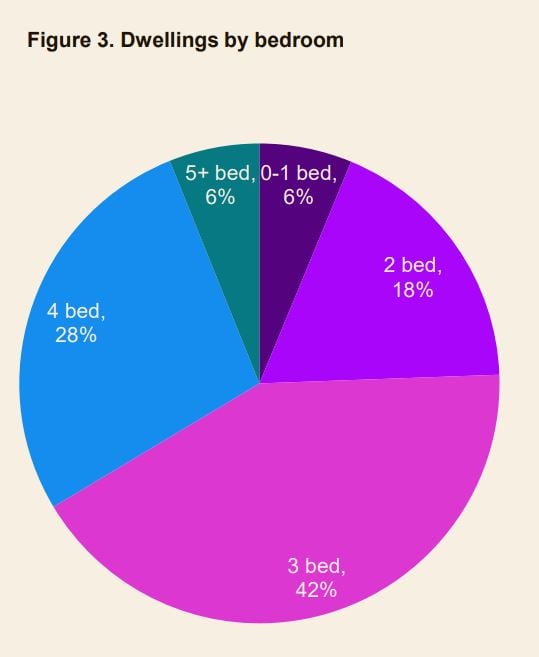

Supply is mismatched: we keep building large family homes on the fringe while demand is growing for smaller, well-located dwellings.

One of the biggest shifts quietly reshaping Australia is the rise of people living alone.

While our headlines are dominated by talk of housing shortages, migration, and interest rates, the reality is that who lives in those homes, and how, is just as important as how many homes we need.

Today, single-person households are the fastest-growing household type in the country.

And this isn’t just a temporary blip; it’s a deep demographic trend that will have ripple effects across the property market, the economy, and even how we build our communities.

For weekly insights subscribe to the Demographics Decoded podcast, where we will continue to explore these trends and their implications in greater detail.

Subscribe now on your favourite Podcast player:

Why living alone is on the rise

Several forces are driving this trend, and together they’re reshaping what a “typical” household looks like.

We’re living longer lives. Australians enjoy some of the longest life expectancies in the world.That means more widows and widowers living alone for 10, 20, even 30 years after their partner passes away. What once might have been just a few years in older age has stretched into decades of solo living.

Marriage and children are delayed. Young Australians are waiting longer to settle down.In decades past, the life cycle was straightforward: leave your parents’ home, get married, start a family.Today, there’s often a 10–15-year gap during which people live on their own, either in shared houses that evolve into solo apartments or directly in single-person dwellings.

“It’s not just that more people are living alone; it’s that they’re living alone for longer stretches of their lives. The traditional life cycle of moving from your parents’ house straight into a family home just doesn’t apply anymore.”

Lifestyle preferences are changing. Independence, privacy, and personal freedom are valued more highly than ever.Many Australians simply prefer living alone, and that choice is easier now thanks to technology, delivery services, and digital social connections.

The housing market impact

Here’s the paradox: even though our household sizes are shrinking, demand for dwellings actually increases.

A single-person household consumes as much housing stock as a family, sometimes more.

Two singles living apart need two kitchens, two bathrooms, two laundries, and two sets of bills.

This is why smaller households drive more housing demand, not less.

And it’s why we’re seeing a structural undersupply in certain types of dwellings.

The biggest areas of demand will be: